Parametric insurance solutions are a megatrend and this market segment will grow massively in the next few years. One reason: digital parametric solutions can be very well embedded into other ecosystems. The potential of this type of insurance is so great that parametric policies could become the "normal" form of insurance in one or two decades. Even today, parametric solutions already make it possible to develop new products and to insure a risk that was previously uninsurable or barely insurable. Due to the new amounts of data that have become available as a result of advancing digitalisation, parametric solutions experiencing a real renaissance.

In our ELEMENT Talk with the topic “Parametric Insurance - Driving change in the insurance industry”, all experts agreed that the future of insurance will be determined by parametric solutions. Gianni Biason (Head Property & Specialty Solutions - Swiss RE), Tim Kaltofen (VP Clients - ELEMENT Insurance), Neta Rozy (Co-founder & CTO - Parametrix Insurance) and Dr. Marcus Schmalbach (CEO - RYSKEX Inc.) give an interesting insight into the current developments in the insurance industry.

For all those who want to deal intensively with the topic, the detailed article on the status quo of parametric insurance offers a good introduction.

Parametric insurance: The future of the insurtech industry?

An insurance policy that automatically pays out a predefined amount when a certain loss parameter is reached - without time-consuming claims management. This is precisely the model that could become the future for many insurance solutions. However, the question remains, will this model replace "traditional" insurance products in the long run? One thing is certain, they are by no means a substitute for traditional covers, such as household content or private liability insurance, but they are a practical model when traditional solutions are not effective, as in the case of various weather events. Equally, they can be used as a supplement to a classic policy.

A parametric insurance policy is based on a previously defined measurand, for example on specific weather data or, in the case of flight cancellations and within transport routes, on time units. Therefore, parametric insurance is often also referred to as an event-based or index-based policy. If a set of objective criteria is met in the event of a claim, the insurance automatically pays out a predetermined amount. All that is required is a measurable index value and the so-called "trigger" that activates the insurance claims process. There is no need for time-consuming claims notifications, checks and cumbersome exchanges between insurer and customer. Of course, this works not only for private individuals, but also for companies, where entire organisations are insured against certain events. The possibilities range from environmental events, e.g., storm or flood damage, to special cyber insurance against cloud outages.

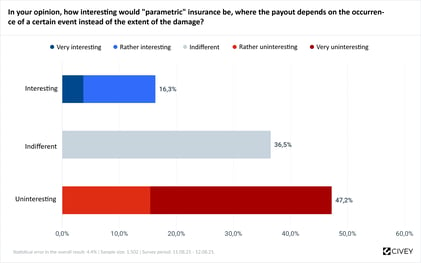

The extent to which parametric policies can be an alternative or supplement to traditional insurance products in the future is currently still largely unknown to consumers. A recent survey* shows that only 16% of participants consider parametric insurance to be an interesting solution at all. The vast majority (47%) do not find parametric insurance relevant for a private household.

Predictability, transparency, flexibility: advantages and use of index-based insurance solutions

Parametric insurance solutions are not new, they have been around since the 1980s. Reinsurers in particular relied on event-based offerings in the past. However, parametric insurance solutions were used almost exclusively to insure natural hazards such as hurricanes, floods and earthquakes or on the capital markets until a few years ago. Nevertheless, they offer a lot of untapped potential for insurers and clients due to technological developments in recent years.

New data sources and advances in data analysis using AI (including machine learning and neural networks) are expanding the areas of application. Parametric policies can be intelligently generated and managed through IoT and blockchain technologies based on global, interconnected events. Whereas damages used to be predicted rather speculatively, the use of IoT and Big Data makes triggers easier to define and probabilities simpler to assess. Customers can benefit from this, especially in the case of large losses or a high number of claimants.

Protection gaps can be closed for previously uninsurable cases and insurers can respond more flexibly to the needs of their customers. The insurance benefit is determined in advance by the customers themselves. By deciding individually which event is to be insured, the threshold value and the respective coverage, customers receive a completely transparent policy. With a smooth and fast payout process, claims settlement and underwriting costs are also reduced for the insurer, as automated processes take effect.

Traditional policies charge adjusters, litigation and claims handling into their premiums without quantifying specific loss amounts. Parametric design eliminates these aspects. The advantages are particularly noticeable in areas that were previously not covered by traditional models.

Cloud outages and pandemic protection: this is where parametric policies take effect

The Corona pandemic is having an impact on the industry. For example, a South African insurance company has introduced pandemic cover that pays a lump sum if the policyholder is hospitalised due to a Covid 19 diagnosis, or any other future pandemic declared by the WHO. The trigger for the benefit is a hospitalisation lasting longer than 48 hours.

Data and its security play an equally important role for society and the economy. Until now, policies have not covered this topic at all or have done so very restrictively, as IT downtimes are difficult to quantify. In cooperation with the US company Parametrix, ELEMENT has developed an insurance policy that covers companies of all sizes against cloud outages. If the outage of the cloud technology lasts longer than agreed in advance, the company receives the fixed sum insured without having to provide elaborate proof of the interruption. E-commerce providers and payment service providers, but also cloud providers themselves, can benefit from this type of insurance. The high economic damage caused by cloud failures, so-called "downtime", was recently made visible to millions of consumers when the social media and messaging services of a large US company were unavailable for several hours.

Parametric insurance: a solution for climate-related insurance claims and much more

Climate change is a much-discussed topic and will play an increasingly important role for the insurance industry in the next few years. The number of fires, earthquakes, droughts, or floods worldwide is increasing every year. The losses are immense and increasingly difficult to quantify. Reinsurers - the experts in this field - estimate that in 2019 around $140 billion in economic losses have been caused by natural and man-made disasters. Conventional insurance policies covered just 40% of the presumed losses. Accordingly, parametric policies offer a major advantage. Whether it is sales and crop losses for farmers due to heat, cold or excessive rain, or the lack of snow in ski resorts - weather stations can authenticate all these "triggers" with data material as the basis for defining the measurable index values. Providers such as Wetterheld insure businesses (including event organisers, restaurant owners, farmers) whose offerings depend on the weather. In times of ongoing climate catastrophes, this is an important aspect.

In conclusion, it can be said that the application scenarios for parametric insurance are diverse. The use and further development of AI, IoT, and sensor technology will continue to grow and open up even more fields for parametric insurance solutions. Parametric solutions can thus come very close to the fit of traditional indemnity products.

The advantages for insurers and insureds are obvious. Providers can now cover risks that have previously been uninsurable. Due to defined triggers, the facts are objective, and the pay-out amount is completely transparent for customers. High costs and discussions due to complicated claims reports are eliminated. For both parties, parametric policies offer a calculable solution with a smooth process should the insured event occur.

*The market research company Civey surveyed 1,500 people between 11 and 12 August 2021 on behalf of ELEMENT Insurance AG. The results are representative of the German population aged 18 and over. The statistical error of the overall results is between 4.2 and 4.5 percent.