The insurance industry is digitalising: Recent technological developments made it possible to add insurance coverage to a variety of third-party products and services. One way of doing so is offering insurance coverage as an add-on service, complementary to the main offering of a company. One of the most prominent (and very classic) examples is travel cancellation insurance when booking a flight. The insurance is simply embedded into the digital sales journey to offer the right product at the right time, it is therefore seen as a contextual annex to the main product.

Also, customers have become more digital in the last decade and now seek insurance solutions that offer more convenience. Think of special warranty insurance when buying expensive electronics because the warranty from the manufacturer ends long before the lifetime of such goods. Thus, insurance products should match the consumer behaviour. New products must be completely digital, available on-demand, easy to administer and seamlessly integrated into all state-of-the-art financing and purchasing options.

Additionally, it is important to keep in mind that regulatory requirements for online insurance sales are currently under a closer look of the authorities. Paid warranty and guarantee promises are a good example, why a partnership with an independent insurer is beneficial. These standard add-ons – at least everybody who have bought a used car knows them – will to a great extent shortly be based on an insurance relationship. In case of used car dealers that means that they need to partner with an insurance company to maintain this service for their customers. So, here is already a need to embed and bundle an insurance product into the core offering, and why not chose a digital one!

Insurance as an add-on or annex offer

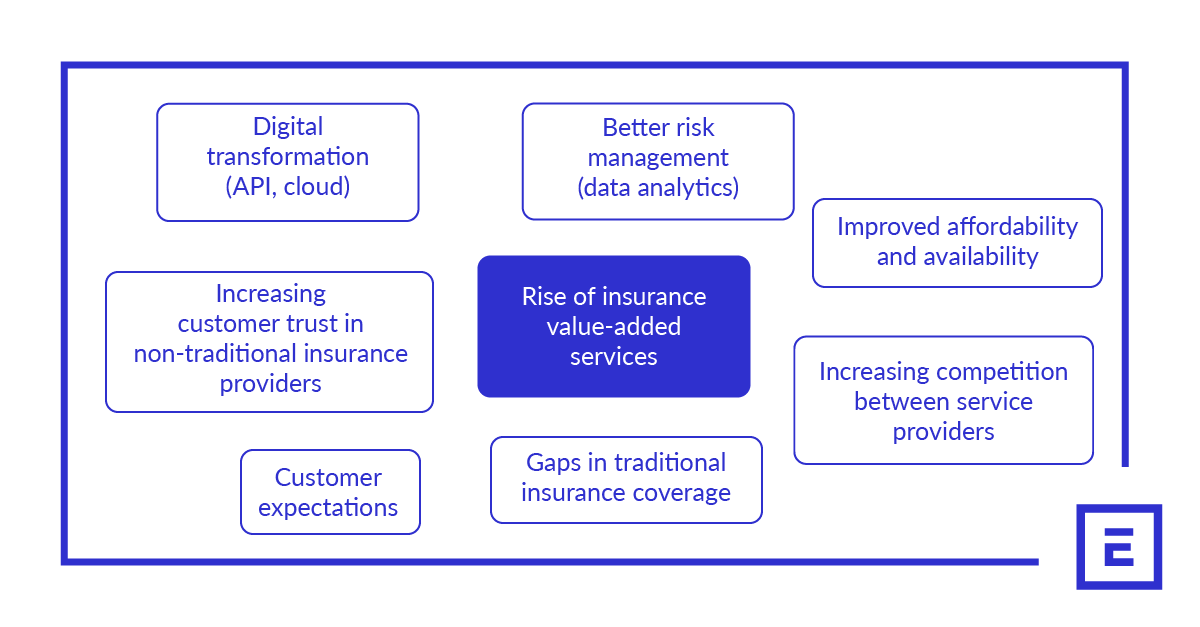

In the face of increasing competition, adding insurance coverage to the main product can positively affect the customer's decision when choosing between two similar products. Already, customers experiencing the trend of value-added services in other financial aspects of their lives. This trend – started by the big internet companies and innovative start-ups alike – has a massive influence on customers and drives the demand for similar services in insurance as well.

As a result, both demand from the customers’ and enterprise side and supply from insurers is beginning to shape innovative insurance solutions of today and outline the products for the future. Furthermore, with more integration of technology into insurance products the type of solutions is beginning to change. From contextual over embedded to parametric solutions a wide variety of new products are emerging. With those additional technological options to build and integrate insurance products into core products of non-insurers, insurance will become more and more part of the customers’ expectation.

Looking at the supplier side digital annex products offer lots of benefits and convenience. Since an add-on insurance can offer more service to the customer – even if they do not choose the cover, they still have the feeling that a whole package is available – an increase of conversion rates can be achieved. Furthermore, the native integration of insurance products into an existing product environment enables additional touch points with customers. From first consultation over claims management to the possibility to add a free insurance cover for a product as a marketing opportunity, customers will reach out. One of the greatest advantages of digital insurance products is the ability to better understand customer behaviour based on the data collected and, as a logical consequence, to optimise the products and the core offerings.

Consequently, the combination of core products with an insurance as an annex, can enable new markets to grow, because customers learn about the products and gain trust in both the brand that is offering a product or service and the added insurance.

Factors affecting the rise of insurance value-added services:

Challenges of selling insurance as an annex to the main product

In case of non-compulsory, add-on type of insurance offering at the point of sale, the purchase decisions of a respective customer depend on many factors. Four areas come to mind that need to be addressed in the right manner, when selling insurance online as an annex. As a first step: Understanding the motivation of customers, but more importantly, a smooth purchase flow for all generational groups. Secondly, it is important to find the right tone to explain the benefits of the insurance and show when the cover is needed. Furthermore, finding the right target group and learn about their needs is a must to address them successfully. Finally, a close inspection of distribution channels because selling insurance online is complex but rewarding – patience is needed.

Selling online

By now everyone in online sales is familiar with the so-called GAFA effect. This development is one of the factors that lately influenced the insurance industry, and in the last years was important for driving change on many levels. One of the main shifts is the possibility to sell and buy insurance online and the rise of digital insurance providers. It opens a vast area of opportunities but also comes with challenges to overcome. Therefore, it is important to understand potential customer’s motivation and buying behaviour. If buying insurance online is a regular activity for digital natives, it can be different for other generational groups. Therefore, offering trustworthiness, patience, support, and an obstacle free buying process are crucial for success in online insurance sales.

Addressing the customer

Finding the right tone to sell an insurance product is key to be successful with a newly launched or customised product, especially if the insurance is bundled with another product. The ease of the process and the explicit contract can play a vital role in customers’ choice of one product over the other. Customers will prefer better fitting products over standard solutions.

Since an insurance policy is a contractual service between the insured and insurer, it involves a legal agreement between both parties which is often hard to interpret for the policyholder. Terms, such as “coinsurance” or “deductible” can hinder a clear understanding for the customer. Therefore, it is necessary to explain all rights and obligations as transparently as possible for the policy holder. This also means explaining the cancellation options and the notification in the event of a claim in a flawless manner. If this is not ensured a customer will most likely interrupt the purchase, become uncertain of taking out the insurance policy, start to gather additional information (if at all), and as an effect the conversion rate will drop.

Finding the right target groups

Combining the main product with insurance coverage can be a great way of customising products and offering more service to customers. For instance, car rental companies can offer flight delay and weather insurance or throw in a deductible insurance as a value-added service. A bike manufacturer may can combine the purchase of a new bike with an insurance against theft. It will save time and costs for customers if they choose one of the options and in case of the newly purchased bike it offers a feeling of safety – especially if you live in a big city. The list of combinations where an add-on insurance cover would come in handy are endless.

By providing a one-stop-shop option, a business can gain a competitive advantage over its rivals. It can be exciting to map the add-on services per specific characteristics of buyers, considering customers’ degree of comfort with the type or number of value-added services. Custom tailored and seamlessly integrated products provide for consumers a holistic online and offline experiences.

Patience during the ramp-up phase

How motivated are people to buy insurance online when bundled with a core product? The complexity of the purchase process and motivational factors affect this decision. Consumers are accustomed to the buying processes at Zalando or Amazon: it just takes a few clicks, and your newly purchased item is on the way. Similarly, purchasing services such as renting a car or booking a flight are quite straightforward.

However, online insurance sales are still more complex than that. Therefore, it is important to pay attention to connect insurance solutions with the right products. It is not useful to just add insurance to any product. The combination must always make sense and offer added value to the customer. Again, a smooth purchase flow is key to successfully sell add-on insurance products, especially if they are natively embedded into your product environment. Customers’ levels of familiarity and confidence about their ability to go through the buying process has a direct effect on sales performance of a company. It takes time to create trust and loyalty.

Do you have any further questions? Feel free to contact us - I am looking forward to hearing your ideas!